I was invited to a Financial Planning Firm’s project party a few months ago held at the Vancouver Fairmont Hotel. The speaker that evening asked the audience, “What’s the ONE THING the Richest People in the World have in common?” I thought to myself, would it be intelligence? A positive attitude? Driven? Hard-working? Perhaps being sociable, relatable or charismatic? There were many success personality traits going through my mind including, “they add value to people’s lives.” Surprisingly, I was wrong; The one thing the richest people in the world have in common has nothing to do with their personality.

According to Bloomberg Billionaires, 17 of the Top 20 Billionaires in the World use real estate as the vehicle to grow their wealth. Is that why we always hear of rags to riches stories of people making it big in real estate and quitting their full-time jobs? Hmmm… Could it be that these people learned the billionaire’s secrets and they took action on that knowledge?

What is it about real estate investing that’s so lucrative? The following reveals the top reasons how people can get rich from real estate investing.

How People Get Rich from Real Estate Investing

CASH FLOW FROM RENTAL INCOME

If you analyse your subject property first before buying to determine if the rental income (greatly) exceeds all expenses of the property, the monthly profits can really add up, especially if you own more than one property.

CAPITAL APPRECIATION

The remarkable thing about real estate is you don’t need to be smart to own. All you need to do is to hold the property for a number of years as historically real estate has doubled in value about every 20 years; so even the biggest dummy can make money doing nothing!

MORTGAGE PAYDOWN

Once again, brains are not required here. Your tenants pay down YOUR mortgage. I’ll never forget Tim Johnson’s definition of a tenant, “Your tenant is a partner in business who will open up shop each morning and lock it up at night. They will look after security & inform you of potential problems in the business. They will cut the grass, rake the leaves, shovel the snow, and pay all the utilities. They will even pay all of your mortgage payments and taxes. Then, in the end, they will relinquish all monetary interest in the business and walk away, leaving you with the profits.” THESE are the reasons why I give my tenants such nice Christmas presents each year; they are the BEST business partners anyone can have!

LEVERAGING OTHER PEOPLE’S MONEY

This is actually my favourite reason for investing in real estate. An example would be; if I buy a property for $300,000, the bank could give me a mortgage of $240,000, or up to 80% loan to value. I then use my home equity line of credit to finance the remaining 20% down payment. I have now effectively leveraged 100% of my property with other people’s money. I don’t know any other investment where the banks are willing and able to finance everything for me, so this is pretty sweet.

But the icing on the cake is this; if my investment property’s rental income covers the interest on my line of credit AND all of the operating expenses, it’s almost like having a license to print money. Knowing this, why would I let my money sit in my principal residence making ‘zero’ when I could have it making me double-digit annual returns? That’s like having an older teenager and allowing them to watch TV all day instead of going to work. It doesn’t make financial sense.

BUYING BELOW MARKET VALUE

There are always motivated sellers in the events of a death, divorce, debt, re-location, or illness. These homeowners are desperate to get rid of their property and will likely sell below market value. Knowing how to seek out these people to help them out of their misery can make you allot of money because you get equity from day one.

VALUE INCREASE THROUGH UPGRADES AND RENOVATIONS

Upgrading areas such as the kitchen and the bathrooms and giving the house a fresh coat of paint can do wonders in forcing appreciation on the property whether your strategy is to ‘buy, fix & hold’ or ‘fix & flip’.

RE-PURPOSING THE PROPERTY

You have a 5-bedroom house that can be rented to a family for $2500 per month. Instead of renting the house entirely, why not rent per room to students for $650/month? The monthly gross rent become $3250, which is $750 more than if you rented the entire house to the family. Most houses have 2 living rooms, so why not turn that living area into two more bedrooms for an extra $1300 per month? But let’s not stop there and rent the covered garage for $100 to one of the tenants. By re-purposing this property as student housing, you make a killer monthly income of $4650, almost doubling the single family rental of $2500. Note: this can be illegal in some municipalities, so do your research before attempting this.

CONVERT USE OF PROPERTY

Similar to re-purposing, an example of converting use of the property would be an apartment building with one title for the entire building. By remodelling, renovating and stratifying the building to condominiums and selling each unit individually, you are able to earn a much higher profit than renovating and selling the entire building.

TAX WRITE-OFFS

Sometimes, it’s not how much money you make but rather how much money you get to keep. Investment real estate is considered a small business, therefore, all expenses incurred to run this business are tax deductible including property management, travel, insurance, property taxes and even meals with partners. What most people don’t know is that when you borrow money from a line of credit to finance an income-generating asset, CRA allows you to write off the interest paid thereby reducing your personal taxes. (I don’t claim to be an accountant, but this is what my accountants advised me.)

So now that you understand how the richest people in the world make their money, I expect to see you on Bloomberg’s Top Billionaires list in the next few years. : )

Teresa Leung is an Investments Realtor specializing in finding income rental properties in areas with outstanding economic fundamentals, and creating turn-key investments for people who prefer to invest passively. She’s a Mentor with UBC’s Sauder School of Business, Community Council Member of Salvation Army’s Kate Booth House, and former Director of Marketing & Investor Relations with Award-winning Real Estate Investment Firm, Alture Properties. You can find her on twitter @TeresaInvestor or www.pointbinvestment.ca. For more information, e-mail Teresa at teresa@pointbinvestment.ca.

Many of you commented on the opportunity cost of the down payment of $110,229 and how you can potentially earn 5-10% annually from investing in a ‘balanced portfolio’ with financial institutions instead.

Perhaps. But maybe you are saying this because you only know what you know and don’t realize what you don’t (yet) know.

I wrote the last article for two main reasons:

99% of so-called ‘Real Estate Investors’ don’t know what a true real estate investment is.

making annual returns of 5-10% from investments is unacceptable, especially when your goal is true financial freedom.

Do you know what a true real estate investment is?

Many investors purchase based on emotions, speculating that the market will appreciate. Like the Bosa condo example in Part I, these people pour hundreds of dollars monthly into their property, and when the housing market crashes, these same Investors panic and sell their properties to avoid further losses. It’s sad for me to see this.

But it’s not really the consumer’s fault. According to Robert Shemin, US Investor and Instructor at Peak Potentials Real Estate Intensive, of all the active Realtors on the market, only 0.02% of them actually specialize in investment properties. And how can you tell if a Realtor is really an Investments Specialist? It’s actually quite easy. All Investment Realtors are also Investors themselves and will likely own multiple investment properties. But the sure-fire way of knowing if a Realtor really does specialize in Investments is by asking them to show you a pro-forma (cash flow analysis) of a property. If they look at you with a glazed look, it’s time to run. Having said that, it’s not the Realtor’s fault people buy ‘emotional investments’ either. Investment real estate isn’t part of the regular Realtor’s school curriculum.

What kind of annual return are you looking for?

I believe that making annual returns of 5-10% from investments is unacceptable and frankly just plain wrong. Trust me Mutual Fund Lovers, after I walk you through the numbers, you just may agree with me.

What does a true investment property look like? (Email me teresa@pointbinvestment.ca for a full report). You can only tell if a property is a true investment after analyzing the numbers, which most Investors and Realtors rarely do.

A true investment property will generate a monthly positive income (cash flow) after paying all the related expenses. This way, even when the market crashes, it wouldn’t affect the Investor at all IF they are not selling the property. Tenants still need a place to live in all market conditions and can’t arbitrarily lower the agreed upon monthly rent. In other words, a true investment property will protect its owner from housing market crashes.

A true investment property will also protect its owner from stock market crashes as it has no direct correlation with other investment vehicles.

Most importantly, a true real estate investment will make the owner money even when he or she is sleeping.

The sample property below is a 2-bedroom 2-bathroom resort-style condo that I sold just over a month ago in the Surrey area of Vancouver’s Fraser Valley. Now some of you may be reading this and think to yourself, “I don’t want to live in Surrey.” And that’s fine because this is an INVESTMENT, and you will likely NEVER live there. As savvy real estate investors, we invest where the numbers work in an area with exceptional economic fundamentals, which is not necessarily anywhere you may want to live in. Successful investors know that there are absolutely no emotions involved in choosing an investment property, as it’s really just a vehicle for income generation.

Now that we got emotions out of the way, let’s get to the fun part of analysing this property.

Property assumptions:

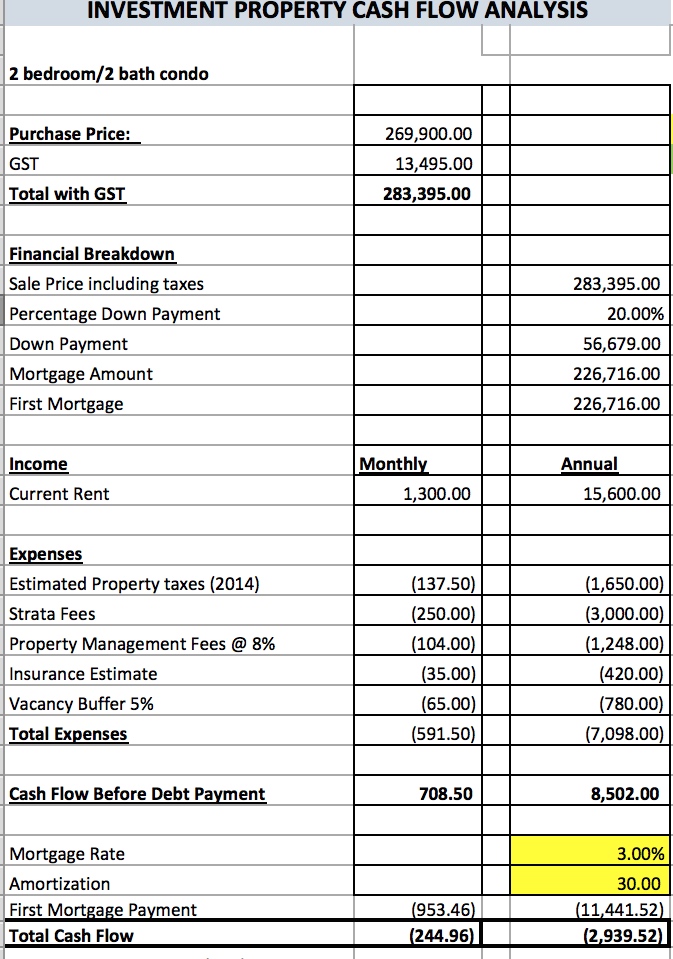

List price of a 2 bed, 2 bath condo is $269,900

From my Craigslist search the average monthly rent for a brand new quality, unfurnished 2 bed 2 bath condo in the Surrey area is $1,300

30 year amortization based on 3% interest rate

20% down payment

Unfortunately, the monthly cash flow is at negative $245 as an unfurnished suite, and this property loses almost $3000 annually.

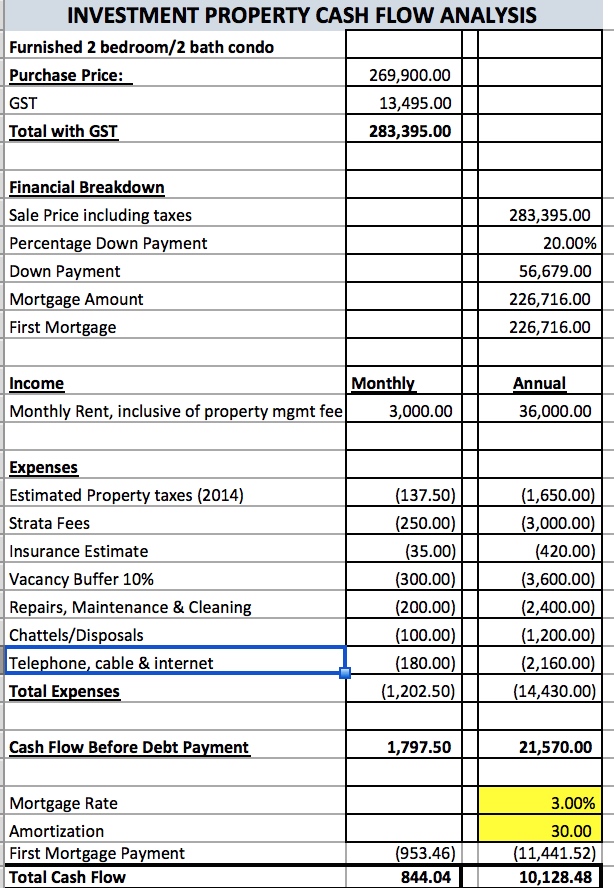

But to be fair to the Bosa condo example, let’s compare apples to apples and see what happens when we furnish this baby and have it managed by a top property management company that specializes in vacation and corporate rentals.

Using the same criteria as the Bosa Furnished suite example, here’s a reminder of the assumptions:

$15,000 for furniture and chattels

Monthly rental income inclusive of property management fees is $3000

Vacancy buffer is now 10%

Repairs, cleaning & maintenance is $200 per month

Chattels & disposables would be $100 per month

Telephone, cable & internet would be $180 per month

All other assumptions remains the same as the unfurnished condo

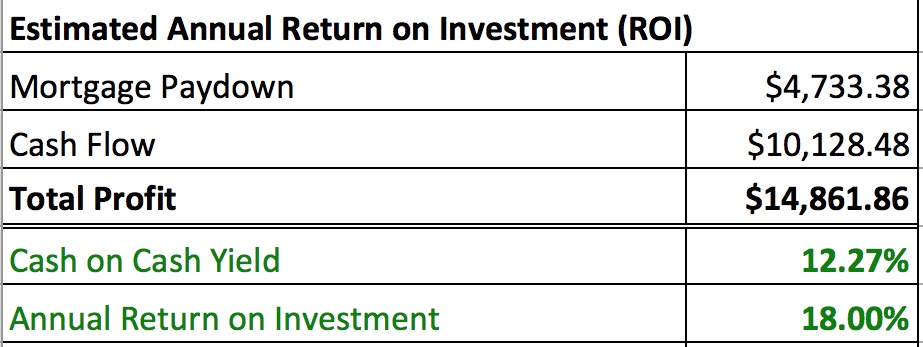

O-M-G! This property now cash flows!!! But what does this mean exactly? Many of the readers from part one of this article mentioned opportunity cost, so let’s examine that. I’ve calculated the total start-up cost for this property to be $82,577, which consists of the down payment, property transfer tax, inspection, reserve funds of $5000, furniture, appraisal, legal and all miscellaneous advertising and closing costs. Since $82,577 is the total cash outlay, I will use this number to calculate this property’s return on investment.

I’ve used the first year mortgage pay down and the annual positive cash flow as income, since mortgage pay down is pretty much a given and positive cash flow is likely going to happen based on the property being managed by experienced managers.

Return on Investment, ROI

As you can see, the initial investment of $82,577 provides a profit of almost $14,900 a year and an impressive 18% annual return on investment. Now when was the last time your investments gave you a predictable return of 18% per annum?

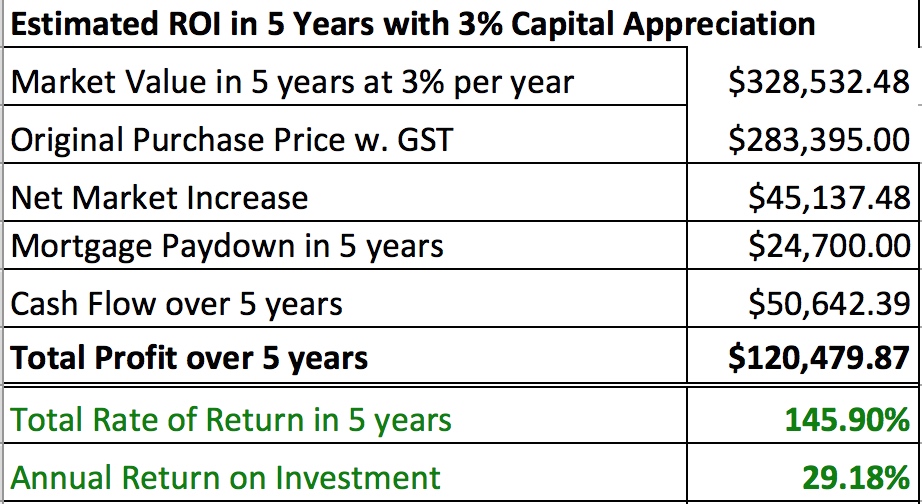

But wait, this gets better. Historically, real estate has doubled in value every 20 years; therefore, it wouldn’t be fair not to include capital appreciation into our analysis. I’ve used 3% appreciation per year just to keep up with inflation, but in some markets such as Fort St. John, BC, and Calgary, Alberta and in some parts of Asia, the capital growth in recent years had been much higher. Based on this assumption, below is an illustration of what would happen to this property in five years.

5 Year ROI

I don’t know about you, but I sure don’t mind making this type of return for doing… well…nothing. Let me explain. We spent $82,577 on the property, we didn’t do a thing after the initial purchase as it’s managed by someone else, and we made over $120,000 in 5 years or 146% ROI. No wonder you always hear of people making millions with real estate. They get this!

Now if real estate investing can provide consumers with such amazing returns, why isn’t everyone and their dog jumping in to invest? Like I said earlier, only 0.02% of Realtors understand investment real estate. Banks and financial advisors don’t sell real estate and it’s the financial institutions that have the multi-million dollar marketing budgets.

This comes to the third reason why I wrote this two-part article. It’s so you, my readers, can join the 1% of Investors out there who do know what a true real estate investment is. It’s so that you can start creating wealth and time freedom today.

So I’m going to ask you the same question I asked in Part I of this article, “For the rest of your life, would you rather make money in your sleep, or work actively for your money trading dollars for hours?” I chose the former. Now you can too!

If you found this article helpful in any way, please share this with your friends and loved ones so that they too, can benefit from this information.

Teresa Leung is an Investments Realtor specializing in finding cash-flowing properties in areas with outstanding economic fundamentals, and creating turn-key investments for people who prefer to invest passively. She’s a Mentor with University of BC’s Sauder School of Business, Community Council Member of Salvation Army’s Kate Booth House, Co-founder of Exceptional Lifestyle Addicts Meetupand former Director of Marketing & Investor Relations with Award-winning Real Estate Investment Firm, Alture Properties. You can find her on twitter @TeresaInvestor. For more information, e-mail Teresa at teresa@pointbinvestment.ca.

Disclaimer: The average annualized capital appreciation on Canadian real estate is above 5.0% per annum since 1980 and 3% scenarios have been used for illustrative purposes only.

E. & O. E. The calculations and assumptions listed above are estimates only, they are not guaranteed., and in no way reflect with absolute certainty the future performance of the property. Purchasers are responsible for performing their own evaluation and forecasts. As with all real estate purchases, actuals may vary due to current and future economic conditions and time. Projections are for illustrative purposes only and are not indicative of anyactual returns or a guarantee thereof. Accordingly, there is no representation that actual results realized will be the same, in whole or in part, as those presented herein. Vacancy rates, inflation rates, appreciation rates, and mortgage rates are subject to market conditions.

I had the pleasure of meeting Jim Bosa, President of Appia Developments, at the Realtor’s launch of Phase II of their North Burnaby Solo District project last month. Appia Developments are one of North America’s premier property development firms within the popular Bosa Group of Companies.

For someone with enormous wealth and success, Jim Bosa is truly an understated gentleman who came across as humble and even a bit shy. He mentioned that he didn’t usually speak at public events, and he graciously agreed to answer a few questions and take a photo for my blog (yes, he really is tall, and I am really this short).

I asked Jim if he thought his condos would make a good investment and he said, “It depends on what you are looking for, but I welcome all purchasers whether they are home owners or investors.” Smart answer. The rest of our conversation was just chatting about the future of North Burnaby and how his company plans to capitalize on the area’s growth.

Before I left the event, I grabbed a price list to determine for myself if buying a brand new condo from Solo District would be a good investment based on cash flow. After all, I am a Real Estate Investor and I’m always looking for good investments. After analysing the numbers, here are my results based on the following assumptions:

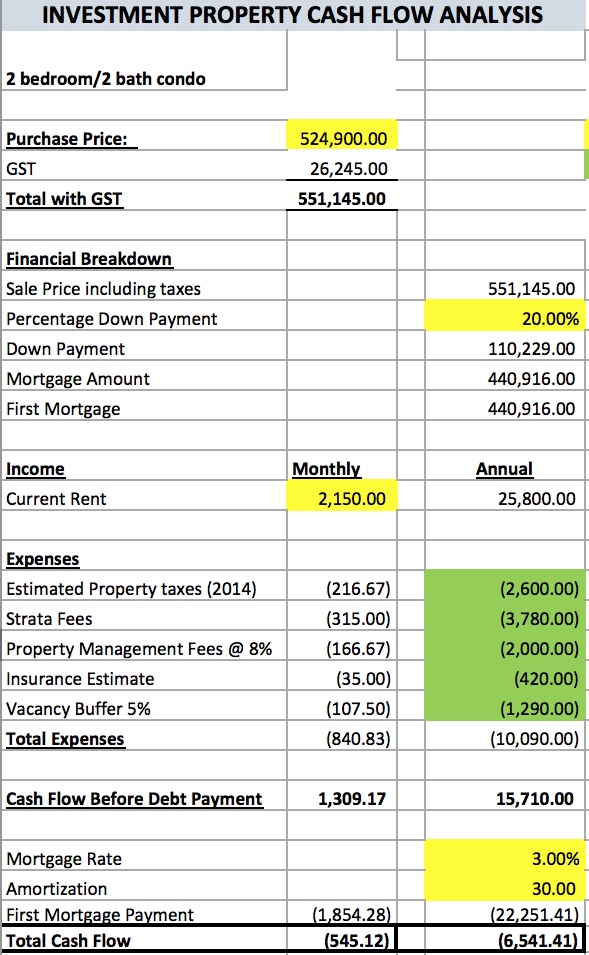

List price of a 2 bed, 2 bath condo is $551,145 inclusive of GST

From my Craigslist search the average rental price for a brand new quality, unfurnished 2 bed 2 bath condo in the North Burnaby area is $2150

30 year amortization based on 3% interest rate

20% down payment

Unfurnished 2bed/2bath Proforma

Unfortunately, the monthly cash flow is at negative $545 and this property loses $6542 each year.

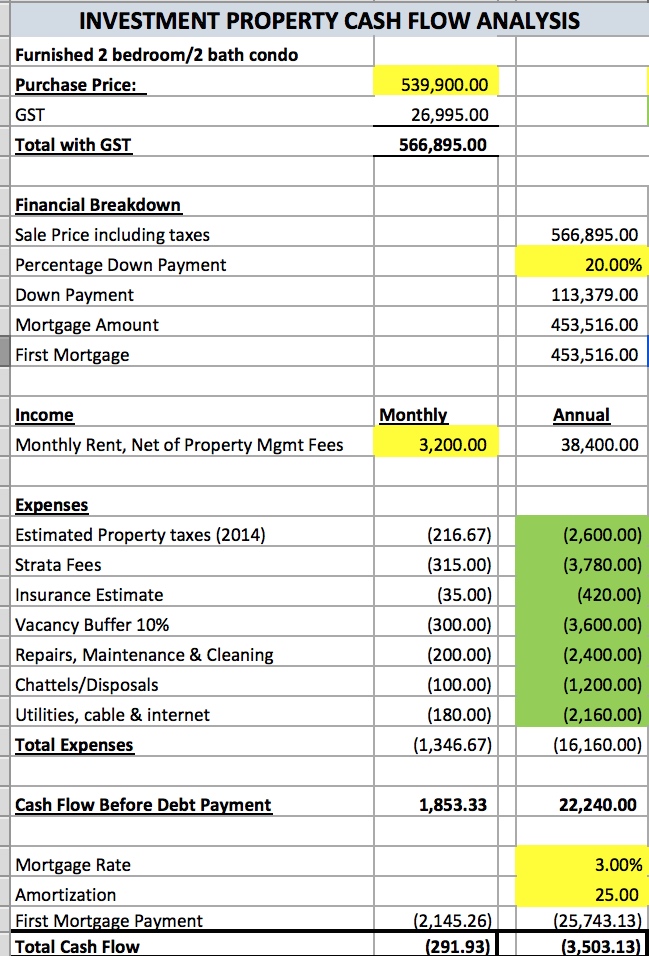

But I really like Jim Bosa, and I want to buy his condo as an investment, so I’m going to increase the monthly income by renting this as a furnished condo, managed by a top property management company with higher profile tenants. By the way, most of the time, when renting out a furnished property, not only do you buy the furniture and chattels, you are also responsible to pay for the utilities since it’s mostly short-term renters. Here are the new assumptions:

Add $15,000 for furniture and chattels (for simplicity sake, I added this to the purchase price and mortgage)

Monthly rental income inclusive of property management fees is $3000

Vacancy buffer is now 10% as furnished can be harder to rent for a full year (unfurnished would be 5%)

Repairs, cleaning & maintenance is $200 per month

Chattels & disposables would be $100 per month

Utilities, cable & internet would be $180 per month

All other assumptions remains the same as non-furnished condo

Let’s see what we get with this new scenario.

Damn, even when furnished, the cash flow is still negative $254 per month with losses of over $3000 annually.

What can I say Jim? As savvy Real Estate Investors, we always invest for positive cash flow first, as opposed to capital growth/appreciation. Therefore, as much as I like you, the North Burnaby area, and the Solo District project, buying a brand new Bosa condo will not get me rich. I’m not just picking on Appia or Bosa, as the same would be true for a brand new condo with Concord Pacific, Wall Centre, Polygon or any developer if rents don’t cover expenses. It’s that simple. The key is to treat your real estate investments like a business and if the projected rents cannot cover all the related expenses, it’s like buying a company that loses money each month. It doesn’t make financial sense.

Now don’t get me wrong, many people look at these new condos as emotional investments similar to buying a brand new Jaguar or Porsche. They’ll never get rich from the purchase, but it sure as hell makes them feel fantastic when they’re in it.

The magic question to ask before investing is, “Are you a Business Owner or an Emotional Investor?” Or better yet, “For the rest of your life, would you rather make money in your sleep or work actively for your money trading dollars for hours?” I choose the former. How about you?

Teresa Leung is an Investments Realtor specializing in finding cash-flowing properties in areas with outstanding economic fundamentals, and creating turn-key investments for people who prefer to invest passively. She’s a Mentor with University of BC’s Sauder School of Business, Community Council Member of Salvation Army’s Kate Booth House, Co-founder of Exceptional Lifestyle Addicts Meetupand former Director of Marketing & Investor Relations with Award-winning Real Estate Investment Firm, Alture Properties. You can find her on twitter @TeresaInvestor. For more information, e-mail Teresa at teresa@pointbinvestment.ca.

I’ve had the pleasure of watching David Chilton speak in person at the Vancouver Investors Forum in November of 2012. For those of you who don’t know David, he is the new Dragon on CBC’s hit TV show, Dragon’s Den, and the best-selling author of “The Wealthy Barber”.

At the end of his speaking engagement, David was kind enough to give us a copy of his latest book, “The Wealthy Barber Returns”. He even talked to us for a few minutes while he signed our books. My impression of David was that he’s a smart and conservative guy who is very knowledgeable about the stock market, investing and saving money.

A few weeks after meeting David, I started reading “The Wealthy Barber Returns” and I must say that I enjoyed the book more than I thought I would. It was an easy read, contained a few chapters that made me laugh and provided a few useful money-saving tips. I completely agree with David’s money-saving ideas and have actually adopted a few of them myself, however most of his book is based on the concepts of “saving up to buy RRSP’s for retirement” and “paying off your principal residence ASAP”. I completely disagree here as David Chilton seems to forget about the opportunity to build wealth through real estate.

(Don’t) Save to Buy RRSP’s for Retirement

The most common RRSP investment products are GIC’s, mutual funds, and stocks. Yes, GIC’s are guaranteed, but they pay extremely low interest rates that barely keep up with inflation. Also, when you invest in mutual funds and stocks, there are no guarantees that you will make money or even retain your principal. Both of these latter investment options give you a highly unpredictable return.

My philosophy is save your money to buy multiple investment properties. When you retire, this option can provide you with monthly passive income so you CAN stop working. You also have the option of selling each property as you need the money. Here are some of the other advantages of investment properties you won’t get with traditional investments:

Leverage. When you purchase an investment property, the minimum down payment is 20% of the purchase price, providing you get approved for the mortgage, the bank will loan you the other 80%. For example if you buy a property worth $200,000, your down payment would be $40,000 and the bank will finance $160,000. Therefore, for a low $40,000 you could own a property worth $200,000. – NICE!

Using Other People’s Money. Providing your property receives positive cash flow (monthly rent collected is higher than monthly expenses) your tenants are paying down your mortgage, your property taxes, your maintenance fees (if strata present), your property management fees (if you don’t manage it yourself), your insurance and all other related monthly expenses! AND you will receive some extra cash or passive income each month. – EVEN NICER!

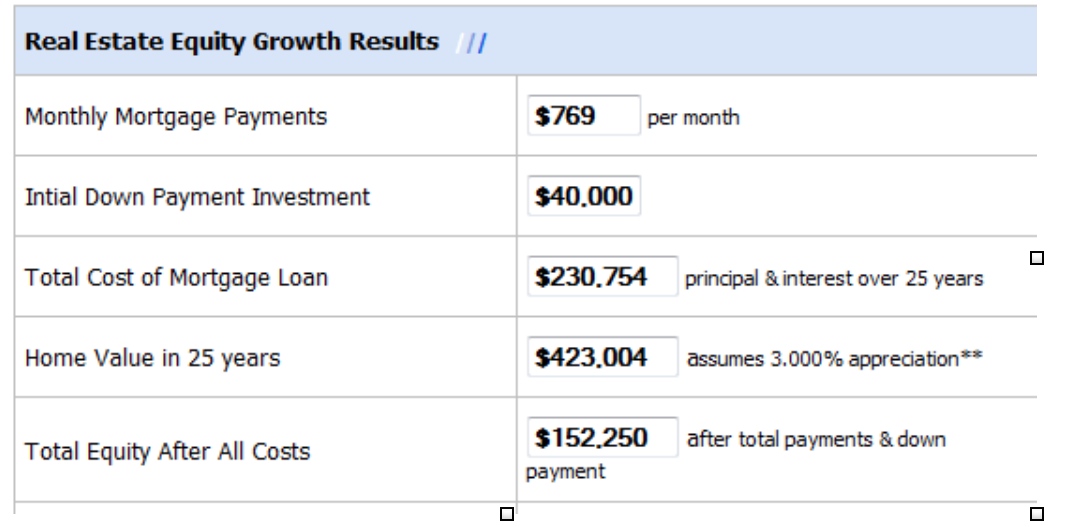

Instant Equity. For the $200,000 property, if it appreciates even at a modest rate of 3% per year, in 25 years time, your $40,000 down payment would then become $423,004 (see table below). Your equity would be $152,250 and your total return on investment after 25 years would be 1057% ($423,004/$40,000). This is not a typo; your profit would be over 10 times over your original investment of $40,000. Now, imagine having 4-5 or more of these babies? – CHA-CHING!

(Don’t) Pay off your principal residence ASAP

A method that sophisticated investors use to expedite the growth of their investment portfolio is to USE the equity in their primary residence towards the down-payment of their investment properties. You achieve this by applying for a Home Equity Line of Credit or HELOC from your bank.

From there, you re-finance your investment properties every 5 years to draw out the equity to buy more investment properties. Why do you do this?

Dead money. Equity sitting in your home doesn’t do anything for you; in other words, your money cannot grow there. Smart money. This is very much like how compound interest works, but at a much larger scale as there are now 3 income centres 1) positive monthly cash flow 2) mortgage pay down by tenants 3) capital appreciation. The first two you can control, the third is unpredictable, however, we know from history that real estate has doubled in value every 20 years. As a bonus, the interest borrowed from your home equity loan are considered to be business expenses since it is borrowed to generate income.

My Recommendation: The sad reality is that most people have to forget freedom 55. Most people will be achieving freedom 75, freedom 85 or no freedom at all. The reason- people just don’t have enough monthly passive income if they stopped working and most of the traditional ‘safe’ investments like GIC’s barely even keep up with inflation. Real estate investing is simple. The buy and hold strategy of real estate investing requires patience and endurance. It will not make you rich quickly. However, through the 3 income centres of cashflow, mortgage pay down, and appreciation, combined with ‘compounding’ your investment properties over time, real estate will get you rich FOR SURE. So David Chilton, care to write your next book with me? Let’s call it “The Wealthy Barber Returns Even Wealthier”.

– by Teresa Leung

If you like this post, please comment below and feel free to share it with friends and colleagues. www.pointbinvestment.ca

I’ve had the pleasure of watching David Chilton speak in person at the Vancouver Investors Forum in November of 2012. For those of you who don’t know David, he is the new Dragon on CBC’s hit TV show, Dragon’s Den, and the best-selling author of “The Wealthy Barber”.

I’ve had the pleasure of watching David Chilton speak in person at the Vancouver Investors Forum in November of 2012. For those of you who don’t know David, he is the new Dragon on CBC’s hit TV show, Dragon’s Den, and the best-selling author of “The Wealthy Barber”.